Traditionally, about 50% of people eligible to collect Social Security at 62 do so. But if you do, you'll receive about 25% less income (i.e. Social Security benefits) than waiting until your full retirement age – between 65 and 67 depending on your birthday. What implication does your early retirement have on your spouse?

Everyone whose work earnings make him or her eligible for Social Security benefits (i.e. income) receives his full Social Security benefit when he reaches his full retirement age (FRA). You can retire as early as 62 but your benefits will be permanently reduced by about 25% from the full benefits you'd get at your FRA. Waiting longer than your FRA to begin receiving Social Security benefits increases your benefits. Waiting to age 70, will increase them by about 32%.

A spouse (i.e. a married person) always has the option of taking the larger of her own working benefit or a 'marriage entitlement' benefit that's based on the benefit her husband collects (assuming the husband was the higher earner in this example).

A spouse's benefits while husband is alive

Since men generally have worked and earned more, it's their wives that are in the position of collecting the larger of their own working Social Security benefits or their social security spouse's benefit.

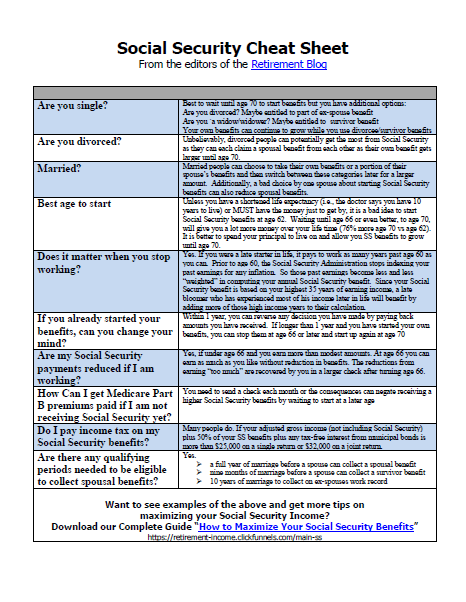

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

| Before You Continue...

Do you know that some married couple have increased their Social Security income with "loopholes" that will close in a few weeks? Get your free coy of the Social Security Cheat-Sheet and learn 4 ways to get a bigger monthly check. |

A wife's spousal benefit can be as high as 50% of her husband's full retirement benefit. To receive this, she must wait for her own FRA and he must do the same.

If he retires early( say age 62), but she waits for her FRA, she still get 50% of her husband's benefit – but his is less because his benefit is reduced due to his early retirement. If he retired at 62, his benefit would be reduced by about 25% from his FRA benefit.

If she retires early at 62, and he waits for his FRA, her spousal benefit will be a reduced about 30% below whatever her 50% spousal benefit would have been. To know more about several ways to increase income in retirement, get the Retirement Guide.

A surviving spouse's benefit

A surviving spouse is entitled to the greater of 100% of the deceased spouse's social security benefits or his/her own working benefit. As stated above, this option is more typical for a surviving wife to make.

Here, the wife's 100% of her husband's benefit is affected by what he actually received. So if he retired early, then her 100% benefit will be smaller to the same extent that his benefit was reduced for early retirement. Her 100% benefit would increase if he delays his retirement to age 70.

So a married man's decision when to collect Social Security has direct implications not only on how much he'll receive in Social Security benefits, but how much his wife and survivor will receive. But remember, there's more to life than financial gain, men don't live as long as women; they deserve some decent retirement time too.

Unless there is some illness that could decrease longevity, it is mathematically advantageous to wait as long as possible to start social security benefits. The various factors that could affect this choice are analyzed in this post. Of course, not everyone has this luxury but if one spouse can wait (the higher earner), both can enjoy more over a lifetime.

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

While a lot of people would wait until 67-70 years to increase their payments by up to 32% - unfortunately this is just not possible for many seniors. Consider the difficulty in finding/keeping employment at that age, in today climate, also the fact that many people approaching this age are physically unable to work in many areas.

You should have listed if the man retires at 65 and woman is under that age does she get full amount she noramly would when he dies. If she does not have social security does it effect what she gets paid.

Best etf funds lits last blog post..Gold double long etf.

The Social Security Administration website at http://search.ssa.gov/search?q=what+every+woman+should+know&btnG=GO&output=xml_no_dtd&sort=date%3AD%3AL%3Ad1&ie=UTF-8&client=default_frontend&oe=UTF-8&proxystylesheet=default_frontend&proxyreload=1 has several booklets about "What Every Woman Should Know" about Social Security.

These booklets, while aimed at women, are basically for spouses, so if you are a man who will be drawing your social security off of your wife's income, then they would apply to you, also.

A must read for everyone.

You have a very informative blog!

The Social Security Administration has a booklet titled, What Every Woman Should Know.

Although the title says it is for women, it is really for spouses, as it will apply to the man if he is drawing social security based on his wife's wages.

This is good Information you provide. and giving the right path to retired people.

What are the widow benefits for a widow under 65 with no children? Is it affected by her husbands earnings?

Getting full Social security benefit seems great. But waiting around 8 years seems waiting time. At the same time it is hark to work at the old ages for advance in age. I don't think i can wait 70 years and it may be difficult for me.

Good article. Not many people think about how much money they looseif they retire early. Not only does it effect the man it can also make a difference on the wifes retirement when he dies.

I am currently 56 years of age. My wife is 60 years of age. She doesn't have enough SS credits on her own to receive her own benefit. I am thinking that at 62 applying for SS and have my wife apply for her spousal benefit. She would be 66 years and four months at that time. Then suspend my benefit before my first check. I am a high wage earner and my wife has spent her time as a housewife raising our children. This strategy looks like how we can maximize our total benefit. I want to work to at least to 63 1/2 and maybe take my benefit at 64 years of age. I may even work a few years longer after I retire from my present job. The freedom to work act of 2000 is doing its job. Without that it doesn't make sense for me to work longer and I work in a field that has sever shortages of qualified workers.

Very good information. I never thought about how it effects my retirement when my husband retires. I think i can choose wich one will be more income so it does not apply to me in this case but i know people it does.

I would be surprised if in the future we even have social security seeing how the government that is currently in control may take that all away and give it to the indigent who do not work.

I am currently a 52 yr old widow my husband would be 56 now, my question is at who's retirement age do I file for his retirement? My age or his age? How do I know when or who's to file for Social Security retirement.

Great article. Thank a lot for the information. Retirement finance is a really good thing. At times people have no clue about it. Thanks for the information. Cheers

Good article. Not many people think about how much money they loose if they retire early. And I never thought about how it effects my retirement when my husband retires. your article got me thinking. thanks a bunch. I need to start working on something for our future. Thanks

Such informative articles... this I never knew "A surviving spouse is entitled to the greater of 100% of the deceased spouse’s social security benefits or his/her own working benefit." My Dad's partner has just passed away and I am sure that nobody has bothered to check any social security benefits.

My wife is 64 and is getting her SS. I'm 63 7 haven't filed yet for mine. Can I file for 1/2 of her value & then later file for my own? I know when I file for my own I'd loose the 1/2 I would be getting of her SS. Please help.

Awesome article. Not many people think about how much money they loose if they retire early. Which I think is a really bad thing in personal planning.

Waiting to receive full benifits from social security is the best option, but for people forced by circumstances to take early retirement it is not always possible. It is really important for people to understand that by waiting they would be much better off. Unfortunately with the economy in such a slump, more and more seniors are being forced into early retirement. Knowing what penalties they face when they can't wait for full retirement is crucial for them to be aware of.

I would be surprised if in the future we even have social security seeing how the government that is currently in control may take that all away and give it to the indigent who do not work..

I actually knew about the spouse right to take over deceased spouse pension. However I came to know about this by a coincidence, because my friend stumbled upon a letter from the pension of her deceased husband. She never knew about this possibility. Everyone should know. Thanks for posting!

Some people stop working before age 62. But if they do, the years with no earnings will probably mean a lower Social Security benefit when they retire.

BTW, good article.

Thank a lot for the information. Retirement finance is a really good thing. At times people have no clue about it. Thanks for the information.

Not many people think about how much money they loose if they retire early. Which I think is a really bad thing in personal planning.

Thanks for the explanation. I would love to retire sooner rather than later, but dread the thought of not receiving all the benefits if I wait to retire at my FRA. As of now, I am saving and investing as much as I can so if I do retire early, or if employer strongly offers an early retirement package, I have something else to pick up the slack.

Is it true that an ex-wife can collect on her ex-husband's Social Security benefits at age 62 and then collect on her own for the full amount at 65?

It makes sense to encourage potential retirees to work longer and reward them for doing so by increasing the pension.

I see the government increasing age limit to encourage the older workers to stay in the workforce and to reduce dependence on pensions to ease the burden on the governments coffers.

This is good Information you provide. and giving the right path to retired people.

What is it that one can sign that prevents you from drawing any money from

x-spouse's retirement?

Thanks for the information. I have advised my parents, who are just over 60, to take a later retirement.

But isn't it a little bit difficult to find a perfect point for both parties' retirement?

Good article. I don't see there are not many people who will think about how much money they will loose if they retire early. Not only does it affect the husband it can also make a difference on the wife's retirement when he dies eventually. And what about all the property and assets that should go to the spouse?

Good writing. Thanks a lot of information. Retirement is a very good thing. Sometimes people do not know this thing. Thank you for the information. cheers

I know too many people that just couldn't wait it out until they hit 65 and it hurt them financially. 65 sure seems like an old age to work until... plan better for retirement is the key. Great post!

Information you provide. and giving the right path to retired people..

Awesome article. Not many people think about how much money they loose if they retire early. Which I think is a really bad thing in personal planning.

very informative post and indeed its important to plan out the retirement well

@ Super Managed Saver - nice point that you mentioned

It's good to see all the facts summarised in one place. Most people don't realise what they have to lose retiring a few yrs early.

I do not see a lot of people no one to think how much money they will lose, if they retire early. It not only can it affect the husband to his wife's retirement, the difference when he finally died. That all property and assets should go to the spouse?

i really agree with this article. we can see the other sight about retire early. yes, we have to have a plan for life. whatever it takes.

I'm glad someone is writing about stuff like this. Its absolutely true and yet, who knew?? I have a family friend that is undergoing this dilemma right now. None of us had any idea of the negative effects of an early retirement.

We find here a real precise information about retirement in a time where that topic is not clearly to be debated among young who have many reasons not to feel concerned even in there more discussed famlily life as divorce rated is increasing and people do not mary anymore.

If I collect $1000 a month and my wife retires early and gets 42%, or $420 a month; does she get $840 a month or $1000 a month when I die? This is assuming she is at full retirement age when I die.

Thanks for such an informative post. I do not think many citizens are aware of such social security policies. Although i would consider it unfair for people to not receive their entire due of social security after retirement. Why would you want citizens to stretch their work life for the sake of security. It can be given to them at a reasonable age with the promised amount.

I never took the subject very seriously up until last year when my husbands mother got retired at 62 and received her SSI.

Thanks for great article, as you can see I am browsing online to find out more about this.

Betty

good information! thank!

this is another reason why I don't rely much of government benefits. I got other insurance and retirement plans with private company. With this I am hoping to still can live the life want even after retirement.

Both husband and wife should retire together and as late as possible to receive the maximum monthly Social Security checks. The same goes for corporate pensions too. The real retirement financial horror story of 2010 and the years to come, is plummeting home values! Go to zillow.com and see what your home is currently worth. Warning you may get sick!

I strongly suggest to my retirement age clients "Sell Your House Now"

Put the money in the bank, move to a local retirement community and buy a small home or condo, then just keep working at your jobs. The big myth is that you should retire at 65 and move to Florida. But by selling your McMansion now and moving to a local retirement home, you will not only get the most cash from your home that you will ever see, you can still keep your jobs, and as a bonus unlike retiring in Florida, you can still be close to your children and grandchildren.

There really is a retirement income. Wherein employees who retire will have benefits like money that can be used for their needs especially when they are getting old.

Hi. This is my first visit to your blog, but I was really impressed with your ideas on the retirement. you put forward a good point, so I decided to advise my parents to take a later retirement. it might be more wiser. Thanks, and I’ll definitely be back !

Well, there won't be any money left in social security since the government is just spending it all.

Are there posts you've made about that issue?

Visualizing the retirement life is essential to plan for it......whether you work or not, you should have some savings for sure

great post,I agree with the way of invest for retirement. It’s a great idea. Maybe everyone has a different opinion for the best sector of investment, but i agree with the idea not to look at the direction of the market to influence the decision.

Some jobs are being outsourced and many are being given to foreign nations via the H1B and L1 visa programs . Eligible guest worker and training program dependents can work in even unskilled positions. The practical training programs available to international students (OPT and CPT) allow companies to employ someone without paying Social Security and Medicare taxes.Between the illegals and the guest workers there are millions of jobs that could be available for citizens if these programs were terminated and illegals were suddenly unemployed by workplace enforcement.When will our government put the US people before politics?

Good and well written article. Never trust the government to provide for you when your pension is due - keep saving money to top of any payment you are likely to receive. I

Its surprising and alerting to know that a spouse’s early retirement may lower other spouse’s social security benefits! Can I do some future finance planning?

I agree, full Social security benefit sounds great. But I do not want to wait so much time...

Waiting to receive full benefits from social security is an option, but for people forced by circumstances to take early retirement it is not always possible. It is really important for people to understand that by waiting they would be much better off. Unfortunately more and more people are being forced into early retirement. Knowing what penalties they face when they can’t wait for full retirement is crucial for them to be aware of.

Social Security benefits should benifit every person. I hope my parents could retire later.

I agree, full Social security benefit sounds great. But I do not want to wait so much time…

Nice post. I guess I never thought about the negative impact early retirement could have on a spouse, but this makes sense. It's one of those Catch 22 situations. Thanks for the useful info - always good to be informed!

Why do people bank on what they expect to get from the government ,start saving money you never can depend on anyone except yourself.Don't wait for the government to prop you up finacially.You never know with whats happening with the economy and it might total disappear and you did plan for it ,then what do you do?

Straight to the point.This must be approved by our local government. Many of our fellow workers need social security purposes. I hope this will be heard from the authorities.

Retirement age is being put up in the U.K By 2012, which is appalling, you will not be able to claim state pension til much later.

I retired from a newspaper in Portland, Oregon (The Oregonian) two years ago. I wish I'd had this info then...

Great article! I never realised you could lose so much money in the process, when you decide to retire early. I'm still young and I haven't really thought about that, but I'll be sure to look into my retirement options though!

seems like it would be worth waiting a few more years for retirement in order to get all of the benefits!

I am just 65 and a high wage earner and I plan to work until I reach 67, my wife is now 63 and she has not worked in 15 years but has worked enough to be eligible for S/S and at FRA should receive around $850. I hear a lot of differing opinions on should she go ahead and retire now. So far I have not been able to find an answer from someone who really knows what they are talking about and is not trying to sell me something, (I do not trust those answers)

Thanks for the useful info.

Social Security benefits should benifit every person.

While clients may have the option of retiring early and beginning to receive social security benefits immediately, the eligibility age for remains at 65. So, although they may be able to replace a sufficient amount of their earned income with social security benefits at age 62, they may not be able to adequately replace their employer-provided health insurance. While recently enacted health care legislation should help this situation, it's too early to tell exactly how much.

Thank you so much for this information on retirement. Im 65 and not getting any younger.

I will be 62 in March. Married 38 years. Was told about the reduction of benefits and that I am entitled to reduced spousal benefits also. Only worked 6 years. Only got notification that I will be getting my first check in May 2011, but no mention of my extra spousal benefits. Was told tha I should get notification (under seperate) cover by mail stating this. Still waiting. I know what I am entitled to, because of various information, and being told by the agent. What is the hangup. Thank you.

Spouse’s Early Retirement May Lower Other Spouse’s Social Security Benefits....thanks for the great information. People need to realize the implications of early retirement and perhaps 25% loss is a good deterrence that working to retirement is a way better option. Cheap Edmonton Hotels

Great blog post! Seems like it is far more beneficial to wait a couple years to retire and get the full benefits. Definitely makes you think about this. But, all in all, the most important thing to do is enjoy life. You only live once.

Thanks for the great article. I'm 65 and looking for more information on this. Do you know of any additional resources? I was especially interested to learn that a wife's spousal benefit can be has high as 50% of her husband's full retirement benefit. Definitely something I hadn't heard until now.

Nice post. I have a negative impact on early retirement, the couple may have seen, seems to think is its meaning. This is a catch 22 situation. Always good to know - thanks for the information!

Hey!! I am completely agree with your blog that spouse’s early retirement may lower other spouse’s social security benefits.But still there is some dependence on retirement age.

What would the benifits for a widow under 65 with no kids?

Good article. I had no idea that your benefits would be permanently reduced if you try to collect them at age 62.

I've been think retirement,and this post give brief information.

Retirement for me is bit weired considereing im still in my twenties. But with how the econemy is nowadays i think its very important to understand how it all works and start planing early. Good article. Power Wheels Jeep. Will come back again to read up on your other article.

In Australia I heard that you can't collect your retirement pension when either one of you (husband or spouse) is still working. This coming from an Australian himself who I had drinks with. That is strange. Anybody can verify that if it's true?

This is good Information you provide. and giving the right path to retired people.

People should be able to take their retirement early for a reduced sum. You work all your life you should have some time left at the end to have some fun before your body goes!

I understand that my spouse can take 50% of my retirement SS if she waits until she is FRA, i.e., 66. However, can she take her SS if she retires at say 63, then switch to "my" 50% when she is 66 (since 50% of mine will be more than hers).

I think every spouse has the right to retire whenever they like, but your post here really make sense, it's kinda not fair to others.

really good path to retired people , people should be able to take their retirement early so they can get even a reduced sum, its important...

My wife is 60 years of age. She doesn't have enough SS credits on her own to receive her own benefit. I am thinking that at 62 applying for SS and have my wife apply for her spousal benefit. She would be 66 years and four months at that time. Then suspend my benefit before my first check. I am a high wage earner and my wife has spent her time as a housewife raising our children. This strategy looks like how we can maximize our total benefit. I want to work to at least to 63 1/2 and maybe take my benefit at 64 years of age. I may even work a few years longer after I retire from my present job. The freedom to work act of 2000 is doing its job.

It high time one starts preparing for retirement.This post is helpful.But what happens if a spouse retires earlier?

If husband retires early (age 63), due to prolonged unemployment, other spouse continues to work for insurance benefits, is younger (age 62), is their combined income still restricted to $34K annually? Is that figure gross, and what is penalty for greater earnings?

In this post modern competitive world to be strategic is very crucial. But for this we need proper guidance. Such insightful piece of writing can only serve this purpose. Thanks and regards.

Kevin Ashwe says:

July 13, 2012 at 12:53 pm

It high time one starts preparing for retirement.This post is helpful.But what happens if a spouse retires earlier

I completely agrees with your comment.

Thanks,

I think most people who initially get “into” web blogging do it for the SEO traffic but after awhile that sole motivation can not sustain quality blogging.

Your post have a unique content.

Very helpful information you have mentioned in your blog.

Thank you so much

Good information provided by you and it giving the right way to retired people. Thank you for nice information for old people.

I and also my friends were digesting the great guidelines from your site and so the sudden I got a horrible suspicion I had not thanked you for them. My young boys are actually absolutely happy to study them and already have actually been enjoying those things. Thanks for truly being quite kind and for opting for this kind of good useful guides most people are really eager to know about. Our own sincere regret for not saying thanks to you sooner.

Fantastic post thanks for sharing!

"Thank you for sharing. I just readout interesting website’s your awesome interesting and informative topic. I really appreciate your thought about it. It’s really so useful for all"

This info is very useful for me, thanks

-Damzak

Very great post. I just stumbled upon your blog and wanted to mention that I have truly enjoyed browsing your blog posts.

Very nice post. I like your blogging techniques and have bookmarked this blog as found it very informative. Keep it up.....!! i love this blog....

Great post. I am a regular visitor of your website and appreciate you taking the

Good information provided by you and it giving the right way to retired people,I am a regular visitor of your website and appreciate you taking the.

Very nice post, I like this article!thanks very much!

hey i;m totaly agree your opinion and your blog thanks for sharing us thanks a lot